Short: Leslie's, Inc. (NASDAQ: LESL)

VIG originally pitched a short on LESL in February of 2023. Since then, the stock has fallen over 58%. The following memo details a condensed version of our investment thesis.

To view the full pitch, please open on a web browser.

Lead Analysts: Roei Zakut, Daniel Li, and Matthew Day

Editors: Martin Aguirre and Chisom Obioha

Investment Overview

Since 2020, LESL has benefitted greatly from chlorine price inflation. However, due to its unsustainable nature, management has concealed chlorine price inflation’s contribution to their sales growth in their investor materials. LESL’s total sales grew by 16.3% in FY 2022, an outlier from their historical growth figures. However, through our analysis, we find that Trichlor, LESL’s chlorine tablet product, makes up ~$184mm of LESL’s sales growth in FY 2022, meaning non-Trichlor sales grew by only 2.7% year-on-year. In their most recent investor presentation, LESL management has issued positive Trichlor sales guidance. The street has taken management’s guidance at face value and is thus pricing in elevated chlorine prices.

Trichlor price increases were driven by temporary factors that are now easing.

In 2020, the Biolab Westlake factory, which produced ~30% of the United States’ supply of chlorine, burned down. This acute supply shock alongside the COVID-19 demand increase for pools and pool supplies (i.e. chlorine), led to an unprecedented surge in chlorine prices.

The Biolab factory has since been rebuilt with 30% more capacity and demand for pool chlorine has normalized. With these factors in mind, we have found with a high degree of certainty that chlorine prices will decrease.

We find that the market is mispricing Trichlor deflation risk to earnings. Consensus forward multiples imply that chlorine supply will keep decreasing, which we find unlikely given the reopening of the Biolab factory.

To understand the effect of Trichlor pricing deflation we looked at the historical correlation between the demand / supply ratio and the NEXANT ECM Chlorine index. This relationship allows us to project out LESL’s revenue through different chlorine pricing and supply scenarios.

As the pool season begins for 2023 (April-September) we project that LESL will miss their H2 earnings as supply increases and demand softens, reducing Trichlor revenue and compressing gross margins.

Company Overview

Leslie’s Inc. is a specialty retail store headquartered in Phoenix that operates in the pool and spa care industry. The company employs 4,200 people and has a network of 990+ brick and mortar stores across the US. They cater to residential and commercial end markets, and sell pool supplies such as chemicals, pool cleaners, filters, pumps, heaters, and more.

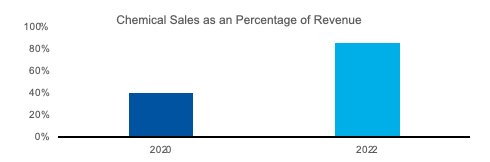

LESL occupies 15% of the $13.8 billion aftermarket pool/spa product spend market. Within the past year, their sales grew 16.3%, a large outlier from their historical growth figures. Within this period, chemical sales have coincidentally grown from 40% of revenue to 80%. We suspect that much of LESL’s recent sales growth is due to unsustainable chlorine price inflation.

Industry Overview

COVID-19 and New Pool Construction

The pool and aftermarket industry has greatly benefitted from the COVID-19 pandemic. During this time, living spaces became of more importance to many homeowners, driving repair and remodeling activity alongside new pool construction. This phenomenon has driven significant excess demand for LESL’s products, and as such created an opportunity for the company to drive abnormal sales growth.

However, we have reason to believe that this demand will subside. Inflation and sub-par macroeconomic conditions have eaten away at the average American’s pandemic savings (3.3% saving rate compared to 16.6% pre-pandemic average). With 63% of Americans living paycheck to paycheck, it is unreasonable for new pool construction to keep growing at its current pace.

Chlorine Price Inflation

While new pool construction provided large growth tailwinds for LESL, we have found that chemical sales have made up the vast majority of the company’s year-on-year growth. This surge in chemical sales is caused by LESL’s ability to take advantage of recent chlorine price inflation, which was in turn a result of increased demand from new pool construction alongside an acute supply shortage.

While this event has provided a large, short-term uplift to LESL’s revenue, our analysis reveals that this growth is unsustainable. The rebuilding of the Biolab factory in November 2022 will shift supply-demand dynamics back to normalized levels, erasing much of LESL’s recent growth. We suspect this aspect of LESL’s business is being obscured by management through convoluted growth metrics and is thus not being priced properly by the street.

Investment Thesis

Point 1: Management Misrepresentation of Chlorine Pricing Impact

Through investor materials, LESL’s management represents sales growth using comparable sales drivers. This means that the percentages displayed are NOT a % of comparable sales, but rather how much they grew relative to last year’s total sales. The formula for dollar sales growth contribution is then as follows: Prior Year Total Sales * Comparable Sales Growth. In the case of FY 2021, Trichlor sales grew $70mm dollars which is ~6% of the previous year’s total sales.

We suspect management leans on this method to represent sales growth as it effectively hides the impact of chlorine price growth upon their revenues.

Knowing this, we can back into LESL’s historical Trichlor sales to estimate the true impact of chlorine price inflation on the company’s revenues.

References:

Chlorine price derived from the NEXANT ECM Index

Total Sales from company financials

Management provides a breakdown of their products' sales growth contribution. In short, the percentage they give is the product's sales growth as a percentage of the prior year's TOTAL sales

2020: We know that a 104% increase in chlorine prices led to a $40mm increase in Trichlor revenue. So $38mm * 104% is equal to $40mm which is management's reporting

2021: Management states that Trichlor sales grew $70mm in FY 2021, $40mm due to price and $30mm due to volume

2022: By confirming that there is a relationship between chlorine price growth and management's representation of "sales growth impact", we can use the index's continued growth of 69% to find that ~$184mm of LESL's revenue growth came purely from chlorine price increases

This point is further reinforced as management has confirmed that Trichlor sales growth has increased 70% year-on-year during Q2 2022 earnings

Taking dollar sales growth from 2022 to 2021, we see that non-Trichlor growth only grew 2.7% year on year, whereas gross revenue grew by 16.3%

We can see that chlorine prices had a large impact on total sales growth during the 2020-2022 period. For example, Trichlor grew from just 3% of revenue in 2020 to 19% of revenue in 2019. Management guidance and the street are assuming that this growth will continue, however, this forecast is suspect as it assumes that chlorine prices must stay elevated.

Point 2: Easing of Chlorine Price Inflation

In 2020, Biolab’s Westlake Louisiana factory burned down. This caused a large supply shock, which when combined with the increase in personal/home pool use over COVID-19, drove up the price of chlorine to unprecedented levels. However, we believe that the re-opening of the Biolab factory for the 2023 pool season and the easing of demand (de-stocking, etc.) will lead to price deflation.

While it will take time for the increased chlorine supply to influence prices, we already see evidence of chlorine price deflation. From the Amazon price history of LESL’s chlorine products, prices have already begun to decrease significantly within the past few months.

From LESL’s most recent earnings call, CEO Michael Egeck stated:

“I don’t think we’re going to see any significant decrease in Trichlor costing. And based on that, I think the industry pricing will hold.”

Despite the clear evidence that chlorine prices are bound to decrease, LESL’s management remains confident in their elevated Trichlor prices. The street has taken this assessment at face value and projected their models accordingly.

Point 3: Mispricing Price Deflation Risk

We fundamentally believe that the street and market are mispricing the impact of chlorine price deflation. To prove this, we projected the impact of chlorine price deflation on LESL’s revenues and compared them to what the street is projecting.

Through reverse engineering, we found a strong relationship between chlorine prices and our synthesized demand / supply ratio. By projecting this ratio, we could then forecast how chlorine prices would be impacted by the increased chlorine supply from the Biolabs ramp-up. Once we forecast chlorine prices, we can project how these price changes would impact Trichlor revenue. In short, the revenue projection methodology is as follows:

Project demand/supply ratio

Utilize historical regression to forecast future chlorine prices

Apply these price changes to Trichlor revenue

Keep non-Trichlor revenue growing at industry average growth rates

Trichlor Revenue + Non-Trichlor Revenue = Total Revenue

1) Demand/Supply Ratio Projections

References:

Demand is represented by the total number of pools in the United States

Chlorine Supply is represented by the total volume of chlorine produced in 1,000 metric tons

References:

From Q2 2024 and beyond, pools were projected using an annual historical CAGR of 2.0%

The BioLab factory was rebuilt in November 2022 with 30% more capacity. Chlorine supply was projected by assuming a target supply in Q1 of 2024E, as historically there is a four quarter lagging effect due to inventory stocking. The target rate was conservatively determined by the pre-explosion peak of 11,918. This number is later sensitized through case analysis.

2) Forecasting Future Chlorine Prices

From the data above, we see that the demand / supply ratio holds a strong correlation with the chlorine index price. Using our forecasted demand / supply ratio, we applied the linear regression function to project the chlorine index price.

3), 4), 5) Projecting Trichlor and Non-Trichlor Revenue

By applying the forecasted chlorine price growth to Trichlor revenue, we can forecast the impact of chlorine price deflation on LESL’s sales.

References:

Derived from dividing total Trichlor sales by units sold. Projected using chlorine price growth figures

Derived from dividing non-Trichlor sales by units sold. Projected using industry CAGR

Derived by multiplying LESL’s revenue by LESL’s sales cyclicality

Total Revenue per Unit multiplied by Implied Units Sold

Market and Street View

By utilizing the goal seek function on the Q1 2024 target chlorine supply to the implied price by the street and market, we can find what their share prices imply about future chlorine supply. To achieve the street projected revenues and consensus share price of $17.50, equity research implies continued chlorine supply DECREASE to 2,074 from the Q1 2023 low of 5,484. The current share price of $13.90 also implies a decrease to 2,937. Due to the rebuilding of the Biolab factory, it is highly unlikely that chlorine supply will continue to decrease. As such, we believe that the market and street are mispricing the inevitable effect of chlorine price deflation.

Bear Case: Target chlorine supply equal to 15,493, representing a 30% greater capacity as cited by BioLabs

Base Case: Target chlorine supply equal to pre-BioLabs explosion levels

Bull Case: Target chlorine supply remains at 5,259

Market and Street Case: “Target Chlorine Supply” numbers are what is necessary to derive their respective share prices from our model

Point 4: 2023 H2 Earnings Miss

As the pool season (April-September) begins, we model a high probability that LESL will miss earnings. Our model assumes that:

The BioLab Factory ramps up chlorine production as expected

Inventory stocking remains at historical levels

Chlorine prices fall more than the street and management are projecting due to historically inelastic supply-demand curve

Chlorine price deflation impacts earnings metrics more than expected due to inconsistent and convoluted financial reporting

We anticipate that LESL management will either miss earnings or be forced to revise their guidance within the second half of 2023. This catalyst will make the market realize the impact of chlorine price deflation on the company’s revenues and reprice the stock appropriately.

Risks & Mitigants

Valuation and Conclusion

Our DCF model is built from a quarterly operating model to account for LESL’s seasonal business model. Our key assumptions include:

Revenues are built from our projection methodology as produced by “Thesis Point 3”

Operating expenses are a projection based on historical quarterly margins. We specifically did not model the effect of chlorine price deflation on margin compression in order to maintain conservatism in regard to our thesis

Capex & D&A expenses were projected according to a PPE schedule of existing and future PPE

NWC was projecting using historical cash conversion cycle ratios

A perpetuity growth rate of 3.0% was utilized as it corresponds with the long-term growth rate for the pool industry

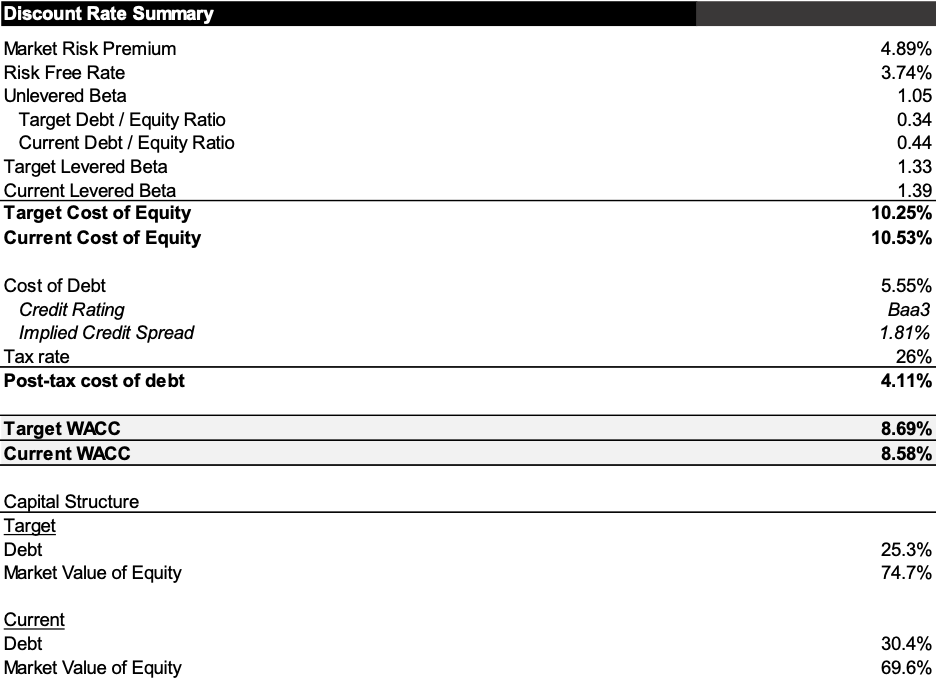

A WACC of 8.7% was utilized according to LESL’s risk profile as outlined in the “Appendix”

From our model, it becomes clear that by properly factoring in the impact of chlorine price deflation, LESL’s current price of $13.90 per share is not sustainable. LESL management and the street have projected revenues with the key assumption that chlorine prices stay elevated. However, through our analysis, we have shown that this expectation is misguided and thus artificially inflates LESL’s share price. The inevitable increase in chlorine supply throughout 2023 will deflate chlorine prices, bringing to light the overvalued nature of LESL’s stock.

Realization of Thesis

The Value Investing Group initially pitched this short on LESL in February of 2023. As of July 14th, LESL management has revised guidance on their FY 2023 EPS estimates from $0.81 to $0.40. Management blamed larger than expected traffic declines, which drove negative comps across both discretionary and non-discretionary categories. Management has also mentioned an inability to manage revenues through price deflation which directly plays into our thesis.

Upon this announcement, LESL’s shares dropped to a low of $5.71 per share (down ~40% from July 13th close).

As a result, the street revised its 2023E earnings estimates.

As of August 2nd 2023, LESL announced fiscal Q3 sales of $611mm (9.3% decrease year on year), and diluted earnings per share of $0.39 (adjusted diluted EPS of $0.41). In reality, chlorine price deflation’s effect on earnings was actually GREATER than VIG estimates. This is because we only modeled the revenue effect of chlorine price deflation without accounting for its impact on gross margins. Additionally, in the Q3 earnings call, management has since admitted to being incorrect about chlorine prices.

“We have seen Trichlor deflation in that category [PRO], and that was a pretty significant headwind to the PRO business in the quarter and year-to-date.”

“I think the PROs went into the season believing that Trichlor pricing should come down, and they were correct.”

By shorting LESL on February 2nd (average price of $13.90 per share), there has since been a 58.9% decrease in the stock’s price to the July 14th low. As of August 14th close, LESL trades at $7.22 per share.

Appendix

DCF | Bear Case

DCF | Bull Case

WACC Calculations

Public Comparables

Seasonality Analysis